Weekly Market Update January 17, 2023

Weekly Market Update January 17, 2023

Presented by Zachary R. Sturdy

General Market News

· The future path of interest rates is uncertain for 2023, but the average Bloomberg surveyed economist expects to see another half percent of increases in the first quarter before levels remain stable through the second and third quarters. Last week’s release of December Consumer Price Index (CPI) data—coming down 0.1 percent, in line with expectations—showed that consumer prices continue to moderate. Signs of softening prices may bolster the case for the Federal Reserve (Fed) to reduce the size of its February 1 rate hike to 25 basis points (bps), but a 50 bps hike is still on the table. Market participants will be looking for signs that more convincingly point one way or the other. U.S. Treasury yields were down across the curve last week. The 2-year, 5-year, 10-year, and 30-year fell 9 bps (to 4.16 percent), 13 bps (to 3.27 percent), 8 bps (to 3.48 percent), and 7 bps (to 3.62 percent), respectively.

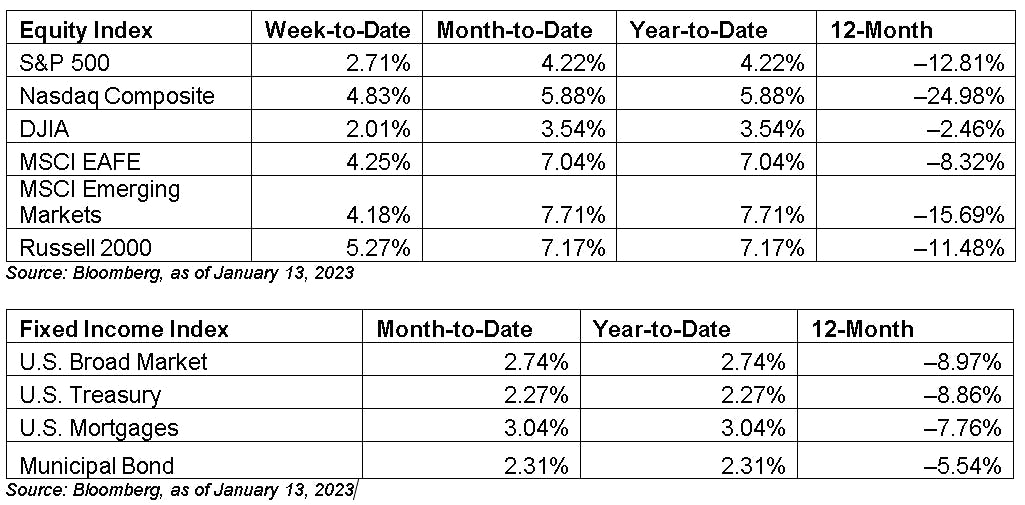

· International, small caps, and growth stocks all fared well last week as continued inflationary cooling has investors looking at a potential pause—or at least smaller rate increases—from the Fed. Support around equities was threefold. Firstly, a continued drop in the December CPI put the year-over-year headline inflation rate at 6.5 percent. This was coupled with the University of Michigan consumer sentiment survey, which indicated consumers’ short-term inflation expectations were for 4 percent and represented the fourth consecutive decline of these expectations. Secondly, we also saw bonds rally since falling inflation means less of the percentage paid via coupons will be eroded via inflation, which lowers the cost of capital. Thirdly, the reopening of China leads to the belief that economic growth may be reaccelerating. The result was a rally for growth and emerging markets, which both benefit from lower U.S. central bank rates and a weaker U.S. dollar. The top-performing sectors last week were consumer discretionary, technology, and real estate. Sectors that lagged were consumer staples, health care, and utilities.

· Last week’s data was focused on inflation and the consumer, with the highlights coming on Thursday with the release of the CPI for December and the preliminary January University of Michigan consumer sentiment survey. Headline consumer prices fell 0.1 percent in December, and year-over-year consumer inflation moderated. This report indicates that tight monetary policy is working to help combat inflation, although there is still work to be done to get price growth back under control. Consumer sentiment improved more than expected to start January, supported by falling short-term inflation expectations that came in below estimates.

What to Look Forward To

This week’s data will focus on the consumer, producer inflation, and housing, kicking off on Wednesday with the release of retail sales and the Producer Price Index reports for December. Retail sales are set to fall in December, which would mark two consecutive months of slowing sales. Headline producer prices are set to fall modestly, which would be in line with the decline in headline consumer prices we saw in December.

Thursday and Friday will see the release of housing start, building permits and existing home sales for December. Building permits are set to increase modestly while starts are expected to decline for the fourth consecutive month. Existing home sales are once again expected to decline, which would mark 11 straight months of declining sales.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million. One basis point is equal to 1/100th of 1 percent, or 0.01 percent.

###

Zachary R. Sturdy is located at 307 S. Front St., Ste: 107 Marquette MI, 49855 and can be reached at (906)226-6056.

Securities and Advisory Services offered through Commonwealth Financial Network, member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services offered through CES Insurance Agency.

Authored by the Investment Research team at Commonwealth Financial Network.

© 2023 Commonwealth Financial Network®