Weekly Market Update January 3, 2023

Weekly Market Update January 3, 2023

Presented by Zachary R. Sturdy

General Market News

· The Federal Reserve (Fed)'s policy rate rang in the new year at a level of 4.5 percent. This came after an historic increase of 4.25 percent over the course of 2022. While the future path of interest rates is far from certain as we ease into the early days of 2023, Bloomberg surveyed economists are anticipating another half percent of rate hikes in the first quarter. Expectations then point to rates remaining stable through the second and third quarters before lowering toward the end of the year. U.S. Treasury yields increased modestly during the final week of 2022. The 2-year, 5-year, 10-year, and 30-year gained 5 basis points (bps) (to 4.39 percent), 1 bp (to 3.98 percent), 11 bps (to 3.86 percent), and 11 bps (to 3.94 percent), respectively.

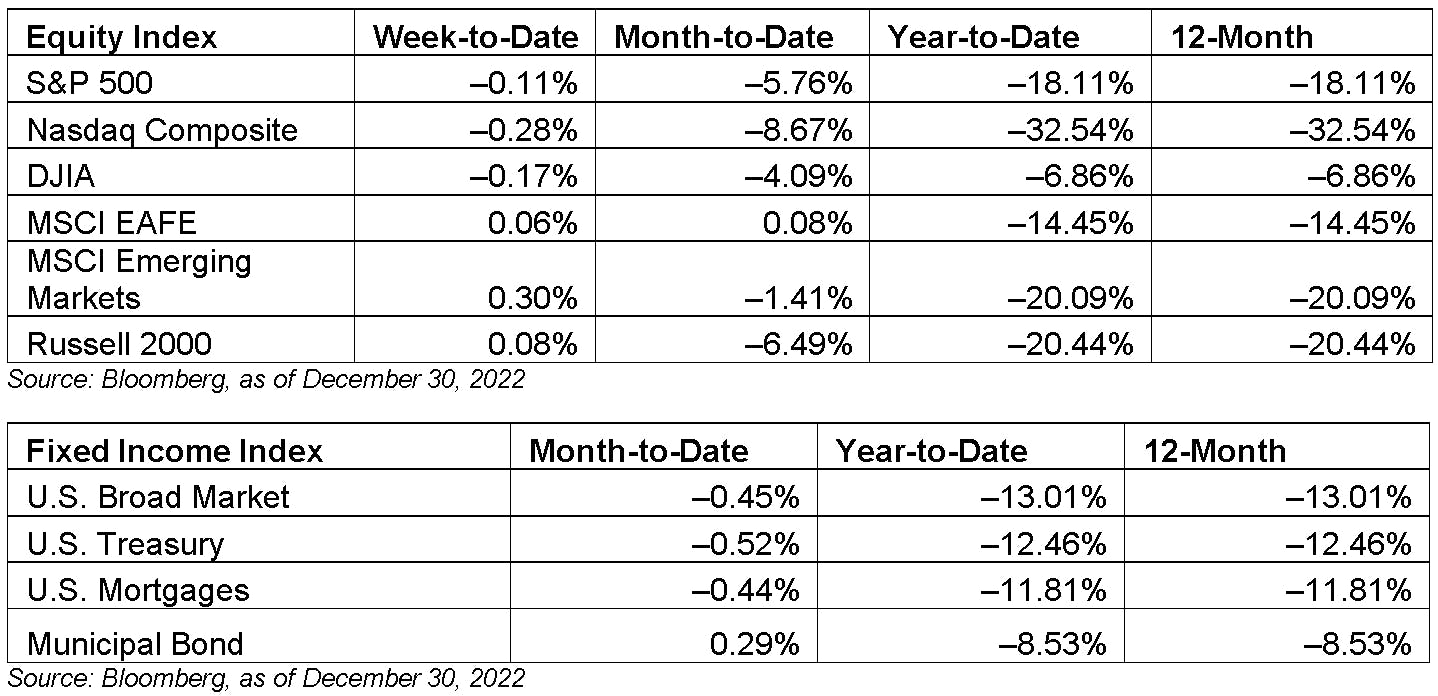

· The last week of the year saw U.S. indices decline, while international indices such as the MSCI EAFE Index and Emerging Markets Index were up slightly. The Russell 2000 was also up slightly and many of these trends were indicative of those seen throughout 2022. The technology-focused Nasdaq Composite Index was among the hardest hit last year as the companies that scaled out quickly in the low interest rate environment following the great financial crisis and in 2020 saw those trends reverse in 2022. Companies such as Amazon (AMZN), Netflix (NFLX), Walt Disney (DIS), and Meta Platforms (META) were among the worst 15 contributors for the S&P 500 index in 2022. These names focused on scaling ahead of profitability in prior years. These names suffered as central banking policy became more aggressive, and the cost of capital rose amid high inflation in 2022. Amazon was focused on scaling its warehousing and ecommerce market share; Netflix scaled out subscribers and viewership, agnostic of who was paying for the service; Walt Disney launched its own Disney+ streaming platform to compete with Netflix; and Meta scaled its Metaverse concept, which continues to be a costly work in progress in achieving its vision for the future of online interaction.

· The Dow Jones Industrial Average, MSCI EAFE, and Russell 2000 fared better in 2022. The energy sector was just one of three positive sectors for the year, alongside utilities and consumer staples. That said, energy was the clear winner with the S&P 500 energy sector up more than 68 percent for the year versus just 2.16 and 0.42 percent in utilities and staples. Other sectors that held up a bit better included health care, industrials, financial, and materials. All three indices carry greater exposure to energy, utilities, staples, health care, industrials, and financials than the Nasdaq Composite. Consumer discretionary was also a major factor in 2022 as these S&P 500 sectors were down by 25.96 percent, 33.93 percent, and 38.56 percent, respectively. We look forward to 2023 to see if these trends will continue and if lower bars for sectors that were down in 2022 will set up easier comparisons in the second half of the year.

· Last week’s data primarily focused on the housing market and the consumer. There were no major economic data releases during the holiday-shortened week.

What to Look Forward To

This week will be full of important economic releases, spanning ISM data to Federal Open Market Committee (FOMC) meeting minutes and the December employment report.

The major economic releases will ramp up on Wednesday with the release of ISM Manufacturing data and FOMC meeting minutes for December. Manufacturer confidence is expected to decline, which would leave the index in contractionary territory to start 2023. The Fed hiked the federal funds rate by 50 bps at its December meeting and signaled a likely slower path of rate hikes ahead, so the FOMC minutes will be closely examined by economists and investors for any hints on the future path of monetary policy.

Thursday will see the release of the international trade report for November. The monthly trade deficit is expected to decline in November following two months with rising deficits.

Finally, Friday will see the release of both the ISM Services and employment reports for December. Service sector confidence is set to fall in December after increased by more than expected in November. The index is still expected to remain in healthy expansionary territory during the month. The December employment report is set to show that 200,000 jobs were added during the month. The unemployment rate is expected to remain unchanged at 3.7 percent.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million. One basis point is equal to 1/100th of 1 percent, or 0.01 percent.

###

Zachary R. Sturdy is located at 307 S. Front St., Ste: 107 Marquette MI, 49855 and can be reached at (906)226-6056.

Securities and Advisory Services offered through Commonwealth Financial Network, member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services offered through CES Insurance Agency.

Authored by the Investment Research team at Commonwealth Financial Network.

© 2023 Commonwealth Financial Network®